So on the recent Monday , the class has ventured to

the last topic of Microeconomics which is

Market Structures. We had go trough initial subtopic in the market

structure to have better acknowledgement in the particular field.

Market

structure

Definition:

- Market is a place where the buyers and sellers meet one another to transact business .

- Market also be defined as an arrangement that facilitates the buying and selling of a product, service, factor of production or future commitment.

- Market structure means the number and distribution size of buyers and sellers in the market of particular goods and services.

Profit maximization in perfect

competition market.

Market

equilibrium is achieved when the marginal cost equal to marginal revenue. Price

is determined based on the average revenue. Prices are fixed in perfect

competition, so marginal revenue is still the same result at a price.

MR=MC

P=AR=MR

Imperfect

competition such as monopolistic, monopoly and oligopoly achieved market equilibrium when marginal revenue equal

with marginal cost. Price are differentiated based on quantity supplied.

MR=MC

P=AR

Types of profit possibilities:

- Supernormal profit.

The profit earned when total revenue is greater than total cost. It also

realized when the price is greater than average total cost.

- Subnormal profit

Economic losses are the

losses incurred because the price is lower than the average total cost or when

total revenue is less than total cost.

- Normal profit

Perfect competition market.

What is perfect competition markets ?

Market in which there are a large number

of buyers and sellers, buying and selling the homogenous products at certain

price levels.

Characteristics.

A) Large number of buyers

There are many buyers in

the market but they cannot control prices. Price is fixed in the market through

the forces of demand and supply. No matter how much has been purchased, price

is always constants. Buyers are said to be price takers.

B) Many sellers in the market

There are many sellers in

the market. Like the buyers they too cannot control price. They are also price

takers. Usually the sellers are small firms. The action of one firm will affect

to the others firms. Example, if the sellers offers a lower price, then he will

incur a loss, and if he sells at a higher price, there will be no demand. In

simplicity, he is powerless in determining price but he can set the quantity he

wants to sell.

C) The product are homogeneous

The goods are homogeneous

and not differentiated. They are identical. The consumer cannot differentiate

whether the goods come from producer A or B or C. Ads is totally absent in this market.

D) Free entry to and exit from the

market.

There must be free entry

to and exit from the market. If the industry is making profits, then new firms

will enter the market. No restriction is imposed.

E) Perfect knowledge

Consumers and producers

have perfect knowledge about the market

situation.

F) Mobility of factors of production.

There must be mobility of

factors of production. There are no barriers to mobility. Land has its own

alternative uses.

G) No transportation cost.

There must be no transportation cost. It is assumed that all firms are situated close to one

another and are very close to the market.

H) Independence in decision making.

There will be no external forces that

will influence the decision of buyers and seller. They make their own

decisions.

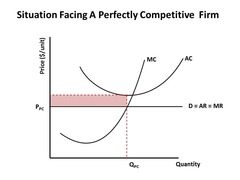

Short run profit in perfect competition market.

In the short term,

perfect competition market has three types of profit which is:

a) Supernormal profit in perfect

competition market.

- The profit maximization occurs when marginal cost equal to marginal revenue.

- The firm earns supernormal profit when average revenue (AR) is greater than average cost (AC).

- The shaded area (EABP) is shown the profit (supernormal profit) area.

- Calculation:

TR=AR x Q

TR=P (x) x Q (y)

TR= xy

TC=AC x Q

TC=AC (a) x Q (b)

TC= ab

b) Normal profit in perfect competition

market.

- The profit maximization occurs when marginal cost equal marginal revenue .

- The firm earns normal profit when average revenue (AR) is equal with average cost (AC). Price is equal at minimum AC, firm at breakeven profit.

- So, the firm will get the normal profit because total revenue is equal with total cost.

- Calculation:

TR=AR x Q

TR=P (x)

x Q (y)

TR= xy

TR= xy

TC=AC x Q

TC=AC (x) x Q (y)

TC= xy

Therefore ,

Profit= TR – TC

=xy - xy

=0

=breakeven

=Normal profit

=Normal profit

c) Subnormal profit in perfect

competition market.

- The profit maximization occurs when marginal cost equal marginal revenue.

- The firm earns subnormal profit when average revenue (AR) is less than average cost (AC).

- So, the firm will get the subnormal profit because total revenue is less than total cost.

- The shaded (EPAB)is shown the subnormal profit (losses) area.

- Calculation:

TR=P (x)

x Q (y)

TR= xy

TC=AC x Q

TC=AC (x) x Q (y²)

TC= xy²

Therefore ,

Profit= TR – TC

=xy – xy²

= -xy

=losses

=subnormal profit